How Much Does a Fast-Food Franchise Cost in 2026?

By Dustin Thompson | Published 2023 | Last Updated: June 17, 2026 | Updated using the 2026 FDD (Issued March 13, 2026)

9 min read

By Dustin Thompson, Franchise Marketing and Development at Jack in the Box | Last updated: July 2, 2026

Once a candidate understands what a restaurant costs, the very next question is "how do I finance a fast food franchise?". I hear it on almost every introduction call I take.

Here is the short answer. Most candidates finance a fast food franchise through some combination of personal liquidity, an SBA backed or conventional bank loan, a retirement rollover, and, where available, franchisor incentive programs that reduce the capital load. The mix depends on your balance sheet, your credit, and how many restaurants you plan to build.

This guide walks through each route, what our own Franchise Disclosure Document says about financing, and what I tell candidates to do before they ever sit down with a lender. Every figure below comes from a primary source: the 2026 Jack in the Box FDD, the U.S. Small Business Administration, the IRS, or the FTC. Each one is linked so you can check my work.

Start with the full number, not the franchise fee. The fee is the smallest check you will write.

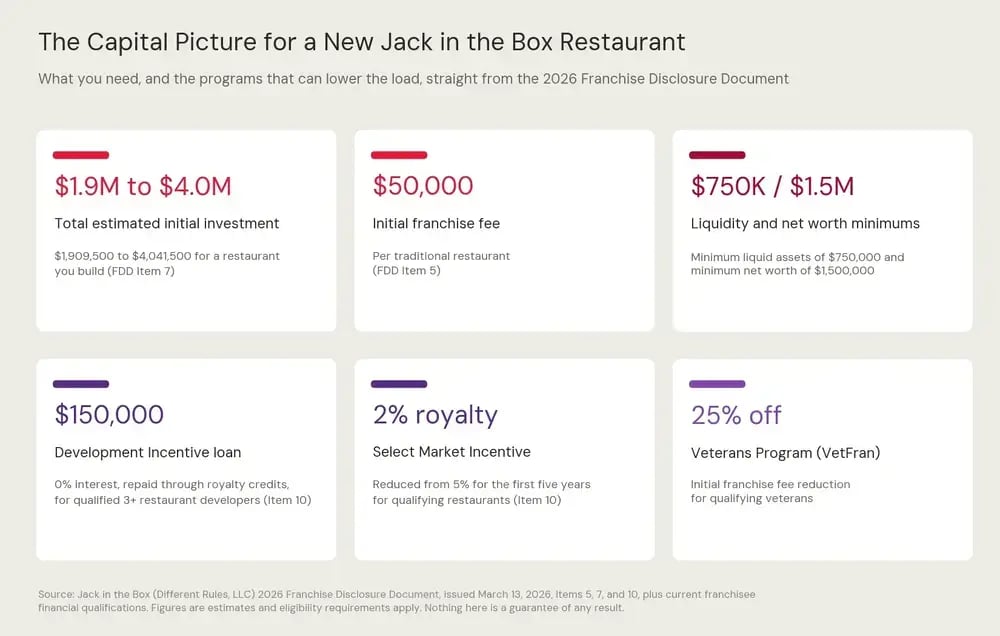

For Jack in the Box, Item 7 of our 2026 FDD, issued March 13, 2026, estimates the total initial investment for a restaurant you build at $1,909,500 to $4,041,500. That range covers land or lease costs, site work, building improvements, equipment, signage, opening inventory, and working capital for the first three months. The initial franchise fee is $50,000 per traditional restaurant. I break the full range down line by line on our franchise costs page.

Financing does not replace qualification. Before any lender enters the picture, we require candidates to show a minimum of $750,000 in liquid assets and a minimum net worth of $1,500,000. Liquidity means cash and assets you can convert to cash quickly. A lender can stretch your capital across a project. A lender cannot manufacture your down payment.

One thing I have seen stall more deals than a weak credit score: liquidity that exists on paper but cannot be verified quickly. Money tied up in a business you have not valued, or spread across accounts you cannot document cleanly, slows underwriting down. Get your liquidity organized before you get excited about sites.

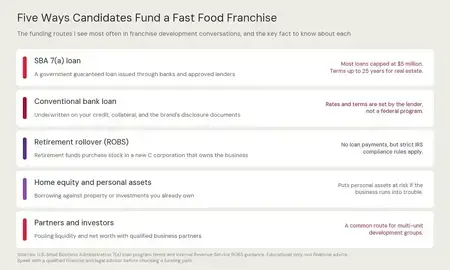

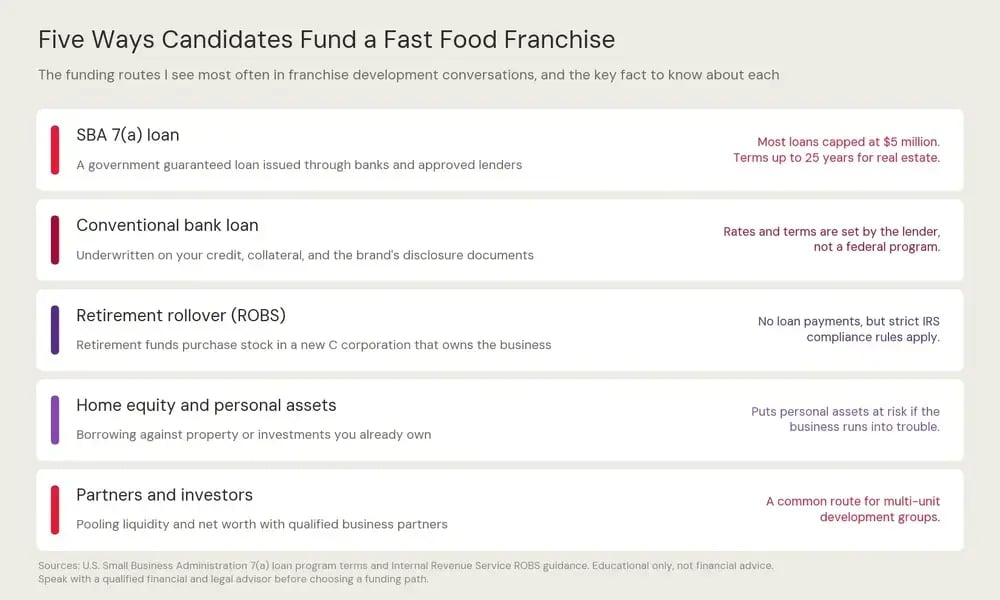

Yes, and it is the route candidates ask me about most.

The SBA 7(a) loan program is the Small Business Administration's primary lending program. The SBA does not lend money directly. It guarantees a portion of a loan made by a bank or approved lender, which lowers the lender's risk and can improve the terms a borrower is offered. According to the SBA's published terms and eligibility rules, most 7(a) loans have a maximum amount of $5 million, repayment terms can run up to 25 years when real estate is involved, and the SBA guarantees up to 85% of loans of $150,000 or less and up to 75% of larger loans.

There is a meaningful change this year. Under a rule announced by the SBA in May 2026, effective July 4, 2026, eligible borrowers can combine 7(a) and 504 loans for up to $10 million in SBA backed financing, double the prior cumulative cap. For a project the size of a freestanding drive-thru restaurant, where real estate and equipment eat most of the budget, that extra room matters.

A practical note from my side of the table. SBA lenders underwrite the franchise system using the brand's FDD, so the document you review during due diligence is the same document your lender will scrutinize. Read it before they do. If you have never opened one, our team walks candidates through the FDD as part of the franchise process, and the FTC publishes a plain language Consumer's Guide to Buying a Franchise that explains what each Item covers.

SBA loans get the headlines, but in practice most candidates I work with assemble capital from more than one source. Here are the five routes that come up again and again in my development conversations.

Conventional bank loans skip the SBA guarantee entirely. Rates, terms, and collateral requirements are set by the lender, and approval usually leans harder on your personal financial strength and operating history. Candidates with prior restaurant P&Ls and strong banking relationships often go this route because it can close faster.

A Rollover as Business Start-up, or ROBS, lets you move existing retirement funds into a new 401(k) plan sponsored by a C corporation, and that plan then purchases stock in the corporation that owns your business. Done correctly, there is no loan, no interest, and no early withdrawal penalty.

I am going to be more direct here than most franchise sites are. The IRS ran a compliance project on ROBS arrangements and describes them as questionable in some respects, with specific concerns around plan administration and stock valuation. The structure is legal when executed properly, and plenty of franchisees across the industry have used it. But you are putting retirement savings into a single operating business, and the compliance requirements do not end at setup. If you go this way, use an experienced provider and have your own CPA and attorney review the arrangement. Not the provider's. Yours.

Home equity and personal assets can bridge gaps, especially for the equity injection a lender requires. The tradeoff is obvious once you say it out loud: you are securing a business loan with the roof over your head or the portfolio you spent decades building. Some candidates are comfortable with that. Others are not. There is no universally right answer, which is exactly why this is a conversation for your financial advisor, not a blog post.

More often than people expect. The liquidity and net worth minimums apply to the ownership group, and I regularly talk with candidates who bring an operating partner, a capital partner, or both. This structure is especially common in multi-unit development, where an experienced operator pairs with investors to build several restaurants on a defined schedule. If you are strong on operations but light on capital, or the reverse, a partnership can be the difference between watching from the sidelines and signing a development agreement.

Not in the way people usually mean when they ask, and I would rather tell you exactly what Item 10 of our FDD says than let you find out later.

The company does not regularly offer financing for new franchised restaurants. In limited circumstances it may offer a build-to-suit arrangement, where the company acquires and constructs the site and then leases the completed restaurant to you at a negotiated rent. And if you ask, we may help you locate a source of financial assistance, at no charge and with no compensation to us for doing so. What the FDD also discloses is that the franchise agreement gives the company a first-priority security interest in the restaurant's business assets, which can affect other lenders, though the company may agree to subordinate that interest to another lender under certain conditions. That is the honest, complete picture.

This is the exception to the no-financing rule, and it is the program I point serious multi-unit candidates toward first. Under the current Development Incentive Program described in Item 10, a qualified developer who signs a development agreement for a minimum of three restaurants, and opens on schedule, may be eligible for a $150,000 loan at 0% interest, paid after ground break and used toward development costs. The loan is repaid by crediting 100% of that restaurant's royalty payments until the balance is retired. No security interest is required for the loan, no third party has to guarantee it, and it can be prepaid without penalty. Eligibility is at the company's discretion and the program can be modified or discontinued, so treat it as a possibility to underwrite around, not a certainty to bank on.

In qualifying Select Markets, franchisees who commit to at least three restaurants under a multi-unit development agreement may see the royalty on each qualifying restaurant reduced from 5% of gross sales to 2% of gross sales for the first five years after that restaurant opens. That is not financing in the lending sense, but it changes the early cash flow math, and lenders notice it when they model your debt service. You can see where we are actively developing on our available markets page.

One more program worth knowing about. Through our participation in the International Franchise Association's VetFran initiative, qualifying veterans receive a 25% reduction on the initial franchise fee. Details and qualification requirements are on our Veterans Program page.

Four things, in roughly this order.

The brand. Lenders read the FDD the way an underwriter reads anything: looking for risk. Item 7 tells them what the project costs. Item 10 tells them what liens the franchisor holds. Item 20 tells them how the system has grown and turned over. A candidate who already knows what those Items say walks into the meeting ahead of one who does not.

Your liquidity, documented. Bank statements, brokerage statements, and a personal financial statement that reconciles. If part of your capital comes from a partner, lenders want the partnership documents too.

Your experience. Restaurant or multi-unit retail operating history strengthens an application. If your background is thinner on restaurants, it helps that new Jack in the Box operators complete a proficiency based training program that runs 10 to 14 weeks before opening. Lenders like to see that the franchisor does not hand you the keys untrained. There is more on our training and support page.

The climate for franchising generally. Lenders also watch the sector. The International Franchise Association's 2026 Franchising Economic Outlook, prepared with FRANdata, projects franchising's economic output growing from $907.3 billion to $921.4 billion in 2026, with roughly 845,000 franchise establishments nationwide. Growth projections are not a promise about any single restaurant, yours included. They are context a loan committee reads.

This is the checklist I share with candidates who tell me financing is their sticking point. None of it is exotic. All of it saves weeks.

When you are ready to talk specifics for your market, the fastest path is to reach out to our franchise development team. We will walk you through the qualification review and the FDD, and if financing is the open question, we can point you toward resources at no charge.

A minimum of $750,000 in liquid assets and a minimum net worth of $1,500,000. These thresholds apply to the ownership group, so qualified partners can combine resources to meet them.

The initial franchise fee is $50,000 per traditional restaurant and is generally due when you sign the franchise agreement. Whether borrowed funds can cover it depends on your lender and loan program, so raise the question early in your lender conversations.

No. The SBA guarantees a portion of loans made by banks and approved lenders, which reduces lender risk. You apply through a lender, and the SBA's Lender Match tool can connect you with participating lenders for free.

It is a legal structure with real tradeoffs. The IRS has published compliance guidance on ROBS arrangements and flags specific administrative and valuation risks. You are also concentrating retirement savings in one business. Review the IRS materials and consult your own CPA and attorney before proceeding.

Not on a regular basis, per Item 10 of the 2026 FDD. Qualified developers committing to three or more restaurants may be eligible for a $150,000 loan at 0% interest under the Development Incentive Program, repaid through royalty credits. The company may also help you locate a source of financing at no charge.

About the author: Dustin Thompson works in Franchise Marketing and Development at Jack in the Box, where he talks with prospective franchisees every week about qualification, capital, and market selection, and works directly from the brand's Franchise Disclosure Document. He writes about franchise costs, financing, and multi-unit development for jackintheboxfranchising.com.

This article is for educational purposes only and is not financial, legal, or tax advice. Consult your own qualified advisors before making financing decisions. This information is not an offer to sell a franchise. Franchises are offered only through a Franchise Disclosure Document, and nothing on this page is a financial performance representation or a guarantee of any result. Figures cited from the Jack in the Box (Different Rules, LLC) FDD are from the version issued March 13, 2026 and may change in future filings. Third party program terms, including SBA loan rules, are set by those organizations and may change.